Tesla’s Earnings: Why the Stock Is Poised for a Sharp Turnaround

It’s no secret that Tesla has achieved a remarkable evolution from a niche electric vehicle maker to a multi-faceted technology company.

Yet Tesla shares have experienced meaningful pressure this year, lagging the broader market amid concerns over slowing vehicle deliveries and margin compression.

Still, as we approach the company’s upcoming earnings report, there’s reason to believe this recent underperformance is a temporary breather rather than the start of a deeper downturn. With several meaningful catalysts on the horizon — from accelerating energy storage growth and Full Self-Driving (FSD) monetization to tangible progress on Optimus and Robotaxi initiatives — Tesla appears well-positioned for a potential near-term rebound.

Digging Deeper into Earnings Projections

The early-year caution around Tesla is understandable. First-quarter vehicle deliveries came in at 358,023 units, missing consensus estimates of approximately 365,000 and marking the second consecutive quarter of softer-than-expected results. This has contributed to a subdued start for the stock in 2026, shedding nearly 14% year-to-date.

Image Source: StockCharts

But Tesla’s long-term story has always been about more than just quarterly vehicle sales, and the upcomingearnings callcould serve as a timely reminder of that broader vision.

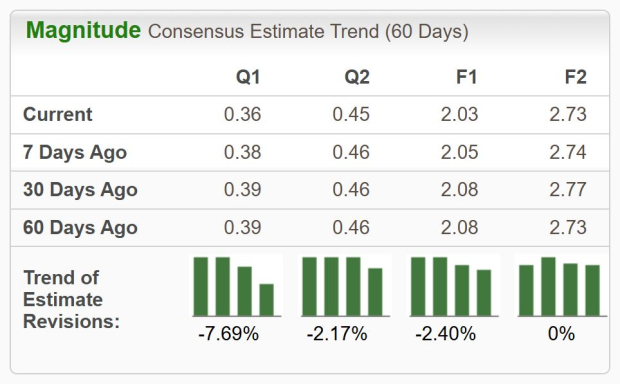

Looking at projected earnings, analysts currently expect Tesla to report first-quarter EPS of 36 cents (up roughly 33% year-over-year), with revenue around $22 billion (+13.4%). These figures still point to solid expansion, particularly when factoring in the rapidly growing energy storage business and software/services revenue streams.

In our view, the market has been overly focused on near-term automotive headline numbers while underappreciating the accelerating contributions from higher-margin segments.

Image Source: Zacks Investment Research

Momentum Builds as Musk Touts Chip Breakthrough

CEO Elon Musk recently revealed that Tesla had completed the design of a new generation of its AI chips for FSD. The company’s “AI5” chip finished the “tape-out” phase, meaning it is now ready for manufacturing. The chip is expected to enter high-volume output in 2027. Musk added that AI6, Dojo3 and other chips are already under development.

One of the other reasons for optimism ahead of earnings is the continued momentum in Tesla Energy. Megapack deployments have been scaling rapidly, with the business now contributing meaningfully to both revenue and profitability. Management has repeatedly highlighted energy storage as one of the fastest-growing parts of the company, and analysts expect this segment to deliver strong double-digit growth through 2026 and beyond.

This diversification is important: while automotive margins have faced pressure from pricing adjustments and mix shifts, energy storage offers higher incremental profitability and more predictable demand tied to global renewable energy adoption.

Equally compelling is the progress on autonomous driving technologies. Tesla’s shift to a subscription-only model for Full Self-Driving has already begun generating recurring revenue, and the company continues to iterate rapidly on FSD software.

Perhaps the most intriguing long-term driver remains Optimus, Tesla’s humanoid robot project. While still in early stages, management has indicated that limited production could begin later in 2026, with broader commercialization targeted for 2027. The potential scale here is enormous — Tesla has long described Optimus as eventually becoming its largest business by far.

Bottom Line

The upcomingearnings callwill likely include updates on regulatory progress, particularly in key markets, as well as early data on Cybercab development. And any tangible updates on development timelines for Optimus could spark renewed enthusiasm.

Tesla TSLA currently carries a Zacks Rank #3 (Hold), reflecting balanced near-term expectations amid the delivery softness. However, the long-term earnings trajectory remains constructive, with analysts modeling continued EPS growth driven by energy, software, and autonomy.

The combination of resilient underlying fundamentals and a compelling long-term roadmap suggests that Tesla’s recent underperformance may ultimately prove to be a healthy breather before the next leg higher.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Tesla, Inc. (TSLA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Discover more from stock updates now

Subscribe to get the latest posts sent to your email.