What Happens If the Nasdaq and S&P 500 Both Fall Into Correction Territory?

Key Points

- Many top S&P 500 components are already in their own individual corrections or bear markets.

- Stocks at lower prices aren’t always good values.

-

Identifying stocks that are down for the wrong reasons can pay off in the long run.

- 10 stocks we like better than Home Depot ›

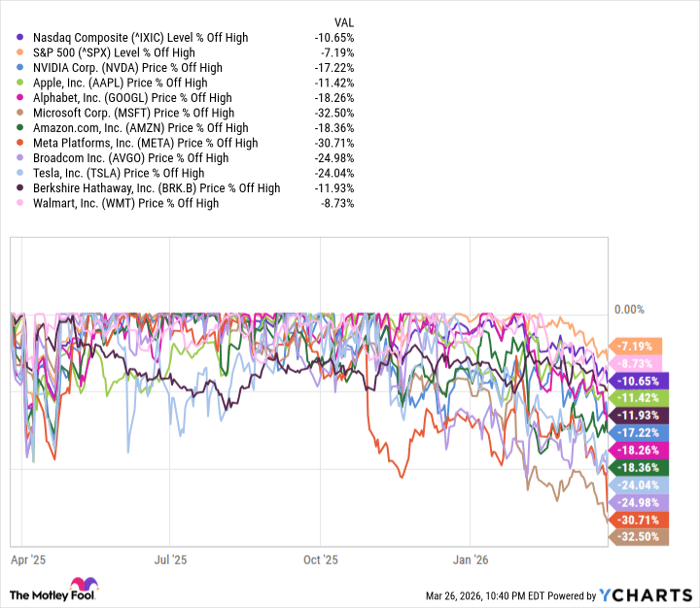

The Nasdaq Composite (NASDAQINDEX: ^IXIC) and S&P 500 (SNPINDEX: ^GSPC) are in the red year to date. The Nasdaq Composite is down more than 10% from its high, while the S&P 500 is 7% off its high.

That puts the Nasdaq into a correction, which is a drop of at least 10% off a recent high but less than 20%. A sustained period in which an index is 20% below its high is known as a bear market. The S&P 500 could be headed there, too.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Here’s why it feels like both indexes should be down even more, and how to find stocks to buy during a correction, as well as ones to avoid.

Image source: Getty Images.

Big names, big drops

This year marks a noticeable step change from the megacap growth-driven market of 2023-2025. Instead of the largest companies pole-vaulting the broader market to new heights, many lower-weighted sectors, like energy, materials, industrials, utilities, and consumer staples, are holding up, while growth-focused sectors are falling.

Here’s a look at the year-to-date performance of the top 10 largest S&P 500 stocks by market cap.

As you can see in the chart, almost all of them are already in their own individual corrections, and four out of 10 of the largest S&P 500 components are down by more than 20% from their 52-week highs. Investors who are heavily exposed to megacap, industry-leading companies may be down far more than the major indexes in 2026.

Corrections can be healthy

The market was extremely top-heavy heading into 2026 — with roughly half of the S&P 500’s market cap tied to just 20 stocks. Since many of these companies are valued more for their future earnings potential than what they are making today, the S&P 500’s valuation was significantly higher than its historical average. In this vein, a correction isn’t the worst thing in the world, and for some stocks, it may be justified.

One of the biggest mistakes investors can make during corrections and bear markets is assuming that, just because a stock is down a lot from its high, it’s a good value. For starters, sometimes stocks can run up too far, too fast, leading investors to anchor to a price that was probably too inflated to begin with. A good example is Palantir Technologies (NASDAQ: PLTR), which is in its own bear market, down 28% off its high.

The company is landing major high-profile deals and growing rapidly, but its stock trades at 122 times 2026 earnings estimates and 86 times 2027 estimates — putting a lot of pressure on Palantir to keep delivering blowout results. While Palantir may be down from its highs, the stock isn’t even remotely on sale and remains worth avoiding.

A far superior approach than chasing high-flying companies is to identify great businesses that don’t need everything to go right to reward patient shareholders.

Buy beaten-down blue chip stocks hiding in plain sight

Companies with a long runway for earnings growth can become too cheap to ignore if they stay beaten down. For example, Nvidia and Meta Platforms are both cheaper than the S&P 500, based on forward earnings, so investors who believe both companies can keep growing are getting a chance to buy these stocks at a bargain. Granted, some investors may be concerned about the payoff of artificial intelligence (AI) investments.

The good news is that there are plenty of top-tier blue chip companies that are beaten down for reasons that have nothing to do with AI.

The Home Depot (NYSE: HD) is a great example, as it’s a well-known nationwide powerhouse. Investors are concerned about declines in consumer spending and a prolonged housing market that has led to sluggish housing turnover and weak demand for home-improvement projects.

But Home Depot is a sleeping giant because it has made key acquisitions during the current downturn — especially in the professional contractor space — that could make it well-positioned to rapidly recover when the cycle turns.

Home Depot is out of favor because impatient investors don’t want to wait for the cycle to turn. But long-term investors can step in and buy the stock for just 22.5 times earnings, which is dirt cheap, given that the valuation is based on trailing earnings from the worst of the current downturn. In the meantime, investors can collect a sizable 2.8% yield from Home Depot, which pays a highly reliable dividend and has raised its payout for 16 consecutive years.

Staying even-keeled during corrections

No one likes losing money. And if the Nasdaq and S&P 500 both fall into correction territory, it will likely mean even more short-term pain.

Smart investors can compound their long-term returns by buying excellent companies at compelling valuations — especially those that are selling off due to fearful sentiment or cyclical factors. Home Depot is one such stock that’s worthy of your consideration.

Should you buy stock in Home Depot right now?

Before you buy stock in Home Depot, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Home Depot wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $497,659!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,095,404!*

Now, it’s worth noting Stock Advisor’s total average return is 912% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of March 27, 2026.

Daniel Foelber has positions in Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Berkshire Hathaway, Home Depot, Meta Platforms, Microsoft, Nvidia, Palantir Technologies, Tesla, and Walmart and is short shares of Apple. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Discover more from stock updates now

Subscribe to get the latest posts sent to your email.