1 Spectacular Stock to Buy Before It Joins Nvidia, Alphabet, and Apple in the $3 Trillion Club

Key Points

- Amazon operates the world’s largest cloud computing platform, which offers a growing portfolio of AI services.

- Amazon’s e-commerce business is increasingly profitable thanks to efficiency improvements in its logistics network.

-

Mathematically, Amazon could join the ultra-exclusive $3 trillion club in less than two years from now.

- 10 stocks we like better than Amazon ›

Ten American companies are valued at $1 trillion or more, but only three are currently valued at at least $3 trillion: Nvidia, Alphabet, and Apple. Microsoft was a long-standing member, but it recently fell just out of contention following a sharp correction in its stock.

I think Amazon (NASDAQ: AMZN) could be the next company to exceed $3 trillion in valuation. Artificial intelligence (AI) is fueling accelerated revenue growth for its flagship cloud platform, Amazon Web Services (AWS), and its e-commerce business is increasingly profitable thanks to growing efficiency in its fulfillment network.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

Amazon is valued at $2.25 trillion as I write this, so investors who buy its stock today could earn a return of at least 33% if the company joins the $3 trillion club. Read on.

Image source: Getty Images.

Revenue growth is accelerating at Amazon Web Services

AWS is the world’s largest cloud platform. It originally provided simple services like data storage, but it has evolved to offer hundreds of solutions that help businesses thrive in the digital age. AWS is now turning its attention to AI, with an expanding portfolio of products and services that include computing capacity, foundation models, and software.

Most AI development happens inside data centers, where advanced chips from suppliers like Nvidia deliver an astonishing amount of computing power. Amazon is one of Nvidia’s biggest customers, but the company also developed its own AI chips called Trainium. The latest Trainium2 chip offers up to 40% better price performance than competing hardware when training AI models, and Trainium3, which just launched, delivers a further improvement of 40%.

AWS Bedrock is where businesses can access ready-made foundation models to help accelerate their AI development. The platform hosts the best models from third parties like Anthropic and Mistral, in addition to the Nova family of models, which Amazon developed in-house. Nova is more customizable than other models, so it’s ideal for building highly specialized AI apps and AI agents.

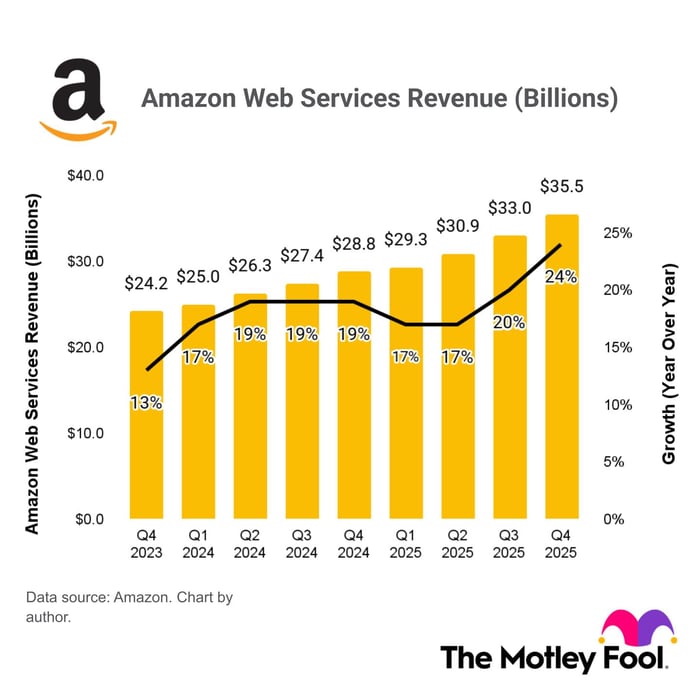

AWS generated $128.7 billion in total revenue during 2025, with momentum steadily picking up throughout the year. The platform produced year-over-year revenue growth of 17% in the first quarter, which had accelerated to 24% by the fourth quarter, primarily thanks to demand for AI services.

Even faster growth might be coming, because AWS ended 2025 with a staggering $244 billion order backlog from customers who are waiting for more data centers to come online, which was up 40% from the year-ago period. Amazon plans to invest $200 billion to build more infrastructure in 2026 to help meet that demand.

The e-commerce business is increasingly profitable

AWS only accounted for 18% of Amazon’s total revenue of $716.9 billion last year, but it was responsible for 57% of the company’s $79.9 billion in operating income. E-commerce remains Amazon’s single largest source of revenue, but it typically operates on razor-thin profit margins because the company wants to offer customers the lowest possible prices.

But in 2023, Amazon overhauled its U.S. logistics network to shorten the distance each order travels, which continues to speed up delivery times and reduce fulfillment costs. During 2025, the company delivered a record 8 billion packages to Prime members in America either on the same day or on the next day, which was up 30% year over year.

Combined with solid growth from AWS, these efficiency improvements are driving significant growth in Amazon’s overall bottom line. The company produced $77.6 billion in total generally accepted accounting principles (GAAP) net income in 2025, which was up 31% from the prior year. That translated to earnings of $7.17 per share.

Amazon has a mathematical path to the $3 trillion club

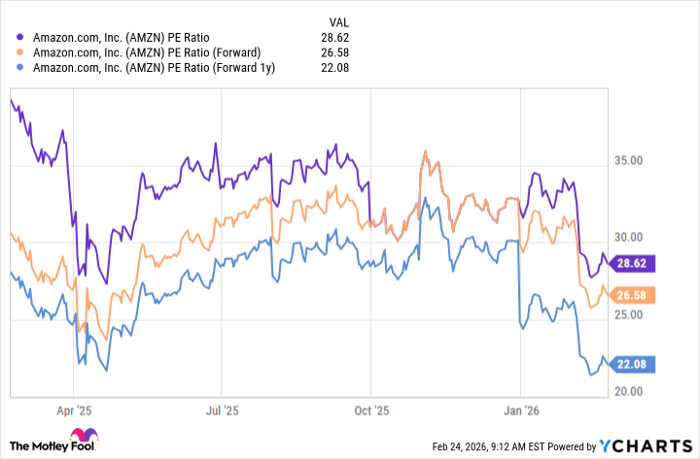

A broad sell-off in the technology and AI space over the last few months has pushed Amazon stock down by 19% from its all-time high. Combined with the company’s strong earnings growth in 2025, its stock now trades at a price-to-earnings (P/E) ratio of just 28.6, which is a discount to the 31.6 P/E ratio of the Nasdaq-100 index. In other words, Amazon looks cheap relative to a basket of its big-tech peers.

But it gets better. Wall Street’s consensus estimates (provided by Yahoo! Finance) suggest Amazon will grow its earnings to $7.75 per share in 2026, and then to $9.39 per share in 2027. That places its stock at forward P/E ratios of 26.6 and 22.1, respectively.

Data by YCharts.

In other words, if we assume Wall Street’s estimates are accurate, Amazon stock would have to soar by 29.4% before the end of 2027 just to maintain its current P/E ratio of 28.6. That alone would nudge its market cap up to $2.85 trillion. However, if Amazon’s stock were to trade in line with the P/E of the Nasdaq-100 (31.6), its stock would have to jump by 42.9% instead, catapulting its valuation to $3.14 trillion.

Considering Amazon’s P/E was hovering at over 35 less than six months ago, I think that outcome is certainly realistic. As a result, Amazon could join the exclusive $3 trillion club in less than two years from now.

Should you buy stock in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $445,995!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,198,823!*

Now, it’s worth noting Stock Advisor’s total average return is 927% — a market-crushing outperformance compared to 194% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 26, 2026.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Microsoft, and Nvidia. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Discover more from stock updates now

Subscribe to get the latest posts sent to your email.